TL;DR – What You Need to Know About Deglobalization

- 🌐 Global trade isn’t dying — it’s shifting, and China’s dominance is being recalibrated.

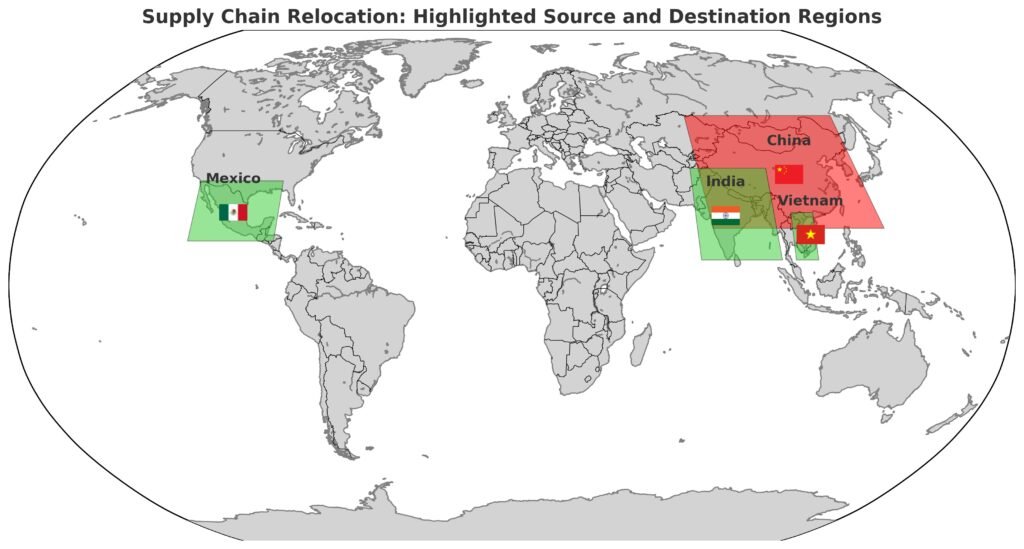

- 🌎 Emerging economies like Vietnam, India, and Mexico are gaining as companies diversify supply chains.

- 🧩 China is still in the game via shadow supply chains and overseas investments.

- 🏛️ Governments are reshaping trade with industrial policy, ESG rules, and origin enforcement.

- 📦 Consumers and companies alike must navigate a more complex but more resilient global economy.

📍 Introduction: The World Isn’t Flat Anymore

The buzzword used to be globalization. Cheap labor, efficient shipping, and cross-border trade turned the world into a just-in-time machine. And at the heart of it all? China. As of 2023, China accounted for over 20% of EU imports, 13% of U.S. imports, and nearly a quarter of Canada’s. For key sectors like electronics, machinery, and consumer goods, China functioned as the planet’s manufacturing backbone.

But that machine started coughing in 2020. First came the pandemic — and with it, the shocking realization that Western nations couldn’t even produce their own masks or ventilators. Personal protective equipment (PPE) shortages exposed how reliant we’d become on overseas production. Then came trade wars, snarled shipping lanes, and semiconductor shortages that brought auto manufacturing to a standstill. All of this culminated in a deeper anxiety: nearly all the world’s advanced chips are made in Taiwan — just a stone’s throw from an increasingly assertive China. It was enough to make governments suddenly remember the word “resilience.”

Welcome to the age of deglobalization — not a total retreat from global trade, but a realignment of where and how companies produce their goods.

What Is Deglobalization, Really?

Deglobalization refers to the slowing or reversal of global economic integration. Companies are:

- Reducing reliance on overseas suppliers

- Reshoring or nearshoring production — meaning companies are either bringing manufacturing back to their home country (reshoring) or relocating it to nearby, often more politically stable, countries (nearshoring) to reduce risk, shorten delivery times, and improve oversight

- Diversifying away from concentrated regions like China

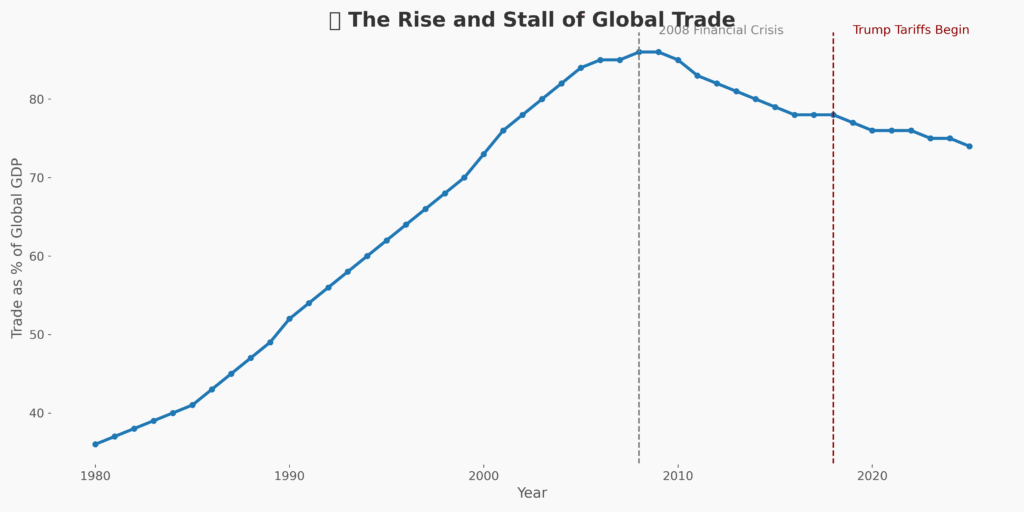

This isn’t just a vibe shift; it’s backed by data. Global trade as a share of world GDP peaked at 61% in 2008. Since 2015, it’s hovered around 52–55% (World Bank). Meanwhile, over 70% of executives say they’re restructuring supply chains post-pandemic (McKinsey).

Why Supply Chains Are Leaving China (and Others)

China’s dominance in manufacturing isn’t over, but it’s changing. Labor costs have tripled over the last 15 years in key industrial regions like Guangdong and Jiangsu, making low-margin manufacturing less viable. At the same time, the U.S.–China trade war imposed tariffs on over $360 billion worth of goods, while export controls on semiconductors and tech gear further strained cross-Pacific relations. Add to that growing concerns over Taiwan — which produces over 90% of the world’s most advanced semiconductors — and you get a recipe for global boardroom anxiety.

Zero-COVID lockdowns added insult to injury. In 2022, entire industrial zones like Shanghai and Shenzhen were shut down for weeks, halting exports, jamming ports, and leaving companies like Apple and Tesla scrambling. The result was a global reassessment of supply chain resilience. Companies now face ESG pressure as well, with shareholders demanding low-carbon footprints and ethical labor sourcing. Suddenly, that single low-cost supplier in China doesn’t look so cheap.

Meanwhile, other traditional hubs like Bangladesh or Malaysia are struggling too — facing labor shortages, rising wages, or unpredictable politics. The era of ultra-concentrated supply chains built on cost alone is fading fast.

Who’s Picking Up the Slack?

As production moves away from China, several emerging economies are stepping up to fill the gap.

China’s New Strategy: Outsourcing… Itself

Here’s the twist: China isn’t giving up — it’s going undercover. To sidestep tariffs and scrutiny, Chinese firms are engaging in a clever sleight of hand:

- Setting up factories in Vietnam, Mexico, and elsewhere — often through shell companies or local partners

- Building Belt and Road industrial parks in places like Egypt, Serbia, and Ethiopia to quietly expand influence

- Maintaining control over critical inputs, machinery, capital, and even management — while labeling the final product with a new country of origin

This tactic, dubbed “shadow supply chaining,” is as hard to trace as it is effective. On paper, goods may appear to be made in a “safe” country like Mexico or Vietnam, but underneath, the design, equipment, and even key operational decisions may still be dictated from Shenzhen or Hangzhou.

For instance, a smartphone may be assembled in a Vietnamese industrial zone, but the tooling, training, software systems, and raw components could all come from Chinese firms. In some cases, even the land is leased through Chinese-owned entities. The result? The product avoids tariffs or political scrutiny, but remains deeply embedded in Chinese supply networks.

Tracking this kind of control is difficult for customs officials and nearly impossible for average consumers. It blurs the line between relocation and rebranding — and it’s part of why deglobalization is so much messier than it seems.

Which Industries Are Shifting Most?

Electronics: Apple now makes one in seven iPhones in India, while suppliers like Foxconn and Pegatron are expanding in Asia and Mexico. But many of these “new” factories are still powered by Chinese expertise, machinery, or capital — a quiet extension of China’s shadow supply chain. For example, Vietnamese plants may handle final assembly, but the automation systems, production tooling, and backend IT often originate in China.

Autos & EVs: Tesla is shifting battery sourcing to North America to qualify for U.S. tax credits. Meanwhile, Chinese firms like BYD are building new plants in Southeast Asia and Latin America, not just to expand, but to get around regulatory hurdles. In some cases, even Mexican-based facilities that appear independent are partially funded or supplied by Chinese entities.

Textiles: Nike, Adidas, and other major brands are relocating operations to Vietnam and Indonesia. However, many of these factories use Chinese-owned upstream suppliers or logistics firms, blurring the lines between actual diversification and rebranded dependence.

Pharma: India’s pharmaceutical exports rose 13% in 2023, especially in APIs, as China tightened regulations. Yet even here, some precursor chemicals still trace back to Chinese manufacturers — proving how deeply entangled the supply web remains.

These developments reveal that while the labels may be changing, the underlying infrastructure of global trade — especially in high-demand sectors — still often runs through China’s economic playbook.

How Governments Are Playing a Role in Deglobalization

This isn’t just about CEOs — governments are pushing the trend.

United States:

The U.S. government has gone all in on reshoring and resilience. The CHIPS Act earmarks over $52 billion to revive domestic semiconductor manufacturing, with Intel, TSMC, and Micron already announcing major U.S. projects. The Inflation Reduction Act (IRA) offers sweeping subsidies to encourage the domestic production of electric vehicles, batteries, and clean energy tech — but with a catch: tax credits are only available if the supply chains are rooted in North America or trusted partners. Meanwhile, the Uyghur Forced Labor Prevention Act (UFLPA) makes it much harder to import goods from China’s Xinjiang region, unless companies can prove the supply chain is clean — a tall order in opaque global networks.

India:

India is deploying its Production-Linked Incentive (PLI) schemes across sectors like electronics, pharma, and solar energy to attract global manufacturing. Apple suppliers such as Foxconn and Pegatron have expanded rapidly in India to meet both local and export demand. The government is also ramping up infrastructure projects — from freight corridors to port modernization — to create a more seamless and investment-friendly ecosystem.

Mexico:

Mexico is reaping the rewards of geography and trade agreements. Under USMCA, its proximity to the U.S. gives it a front-row seat in the nearshoring trend. Global automakers are expanding their manufacturing bases in northern Mexico, while electronics companies set up distribution and logistics hubs to service the U.S. market faster and cheaper. Industrial parks in states like Nuevo León and Coahuila are seeing record occupancy as foreign capital flows in, reshaping the North American production map.

Can the West Counter China’s Shadow Play?

Yes — but only with enforcement and creativity. Combating China’s shadow supply chains isn’t about shutting down trade — it’s about outmaneuvering opaque practices with transparency, traceability, and smart diplomacy.

- Tighter rules of origin: Many Chinese goods enter Western markets with altered country-of-origin labels. Robust enforcement, supply chain audits, and digital tracking tools are needed to verify where products — and their core components — actually come from.

- Transparent ownership reporting: Shell companies and joint ventures often obscure Chinese ownership or control. Western regulators can require disclosure of beneficial ownership to detect hidden influence.

- ESG and labor audits abroad: Mandatory reporting on environmental and labor standards, even in foreign subsidiaries, would raise the compliance bar — and expose inconsistencies in supposedly “relocated” supply chains.

- New trade deals with trustworthy partners: Strengthening agreements with countries like Vietnam, India, and Brazil creates viable alternatives — though with important caveats. In Vietnam’s case, while trade ties are valuable, policymakers must remain vigilant about the extent of Chinese upstream control. Strategic partnerships should be coupled with transparency initiatives and investment screening to ensure that the diversification is genuine, not just geographic.

The West can’t stop globalization — but it can rewrite the rules to favor resilience, accountability, and genuine diversification.

What Deglobalization Means for You

For companies: Expect more complex logistics, regional compliance requirements, and tougher ESG scrutiny. The era of just-in-time delivery is giving way to just-in-case redundancy. Businesses that once prioritized ultra-lean supply chains now face a new mandate: build for resilience. That means sourcing from multiple regions, building strategic reserves, and investing in local partnerships — all of which demand new capabilities across procurement, legal, and operations.

For investors: The redistribution of global manufacturing is reshaping capital flows. While the China growth story once dominated emerging market portfolios, attention is now shifting toward frontier hubs like Vietnam, India, and Mexico. In 2023, Vietnam’s FDI surged by 32%. India brought in over $70 billion in foreign investment, while Mexican industrial parks reported record demand near the U.S. border. Investors don’t need to chase individual countries, but they do need to stay alert to how policy incentives, labor dynamics, and infrastructure upgrades are redrawing the map of global opportunity.

For consumers: You may still see “Made in Vietnam” or “Assembled in Mexico” — but the real origin of many components may trace back to Chinese capital, equipment, or know-how. Still, diversification efforts matter. When Western companies invest in alternative sourcing and forge new partnerships, they help raise labor standards, promote transparency, and stabilize fragile economies. Over time, that creates a more balanced and secure global supply system — one that’s better equipped to absorb shocks without leaving shelves empty.

Deglobalization is messy. But it’s not collapse — it’s adaptation. And that makes the system more complex, but also more resilient.

Conclusion: Deglobalization Isn’t Death — It’s Recalibration

Globalization isn’t collapsing — it’s getting restructured. The age of chasing the cheapest labor or largest factory cluster is giving way to one focused on resilience, trust, and transparency. We’re no longer optimizing for efficiency alone, but for stability and strategic alignment.

That means supply chains will be messier. Products might take a little longer to ship. Compliance costs will rise. But the end result is a more shock-resistant system — one less likely to be paralyzed by pandemics, port closures, or geopolitical standoffs.

Deglobalization isn’t about building walls — it’s about redesigning bridges. With more pillars underneath them.