Economists have a lot of ways to define US recessions, but the simplest version? It’s when the economy throws a tantrum. Officially, a recession is a significant decline in economic activity, lasting more than a few months, and visible across GDP, employment, industrial production, and retail sales.

In the United States, recessions are declared by the National Bureau of Economic Research (NBER)—a group of economists who wait until everyone knows we’re in a recession before telling us. Thanks for the heads-up, guys.

In this article, we’re diving into the history of US recessions over the past 50 years. Think of it as a guided museum tour through economic meltdowns—with a little sarcasm, a lot of facts, and some helpful visuals along the way.

1973–1975: The Oil Crisis and Stagflation Spiral

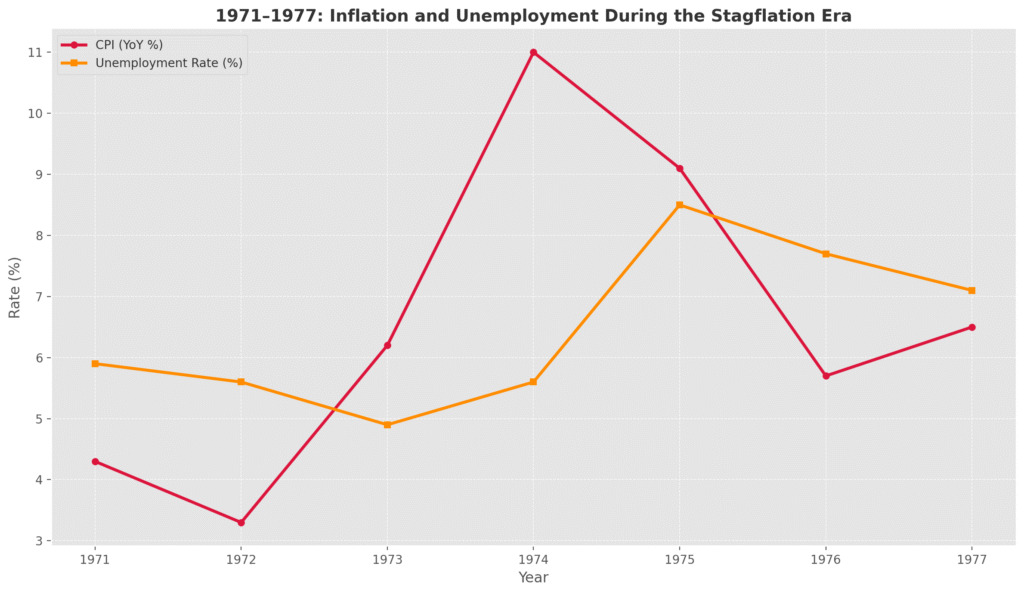

You know it’s bad when inflation and unemployment hold hands and skip through the economy together. Welcome to stagflation. It’s the unfortunate economic combo of high inflation and high unemployment, where prices rise but paychecks don’t—and job openings vanish like your favorite discontinued cereal.

- Causes: OPEC oil embargo that sent fuel prices soaring, sparked by the 1973 Yom Kippur War when Arab nations cut off oil exports to the U.S. in retaliation for American support of Israel, Vietnam War spending that bloated the federal deficit, wage-price controls that tried (and failed) to freeze inflation like a broken thermostat, and President Nixon taking the U.S. off the gold standard—effectively ending the Bretton Woods system. By severing the dollar’s link to gold, Nixon allowed the money supply to expand freely, contributing to mounting inflationary pressures. The result? An economy stuck in neutral with both gas and groceries getting more expensive by the day.

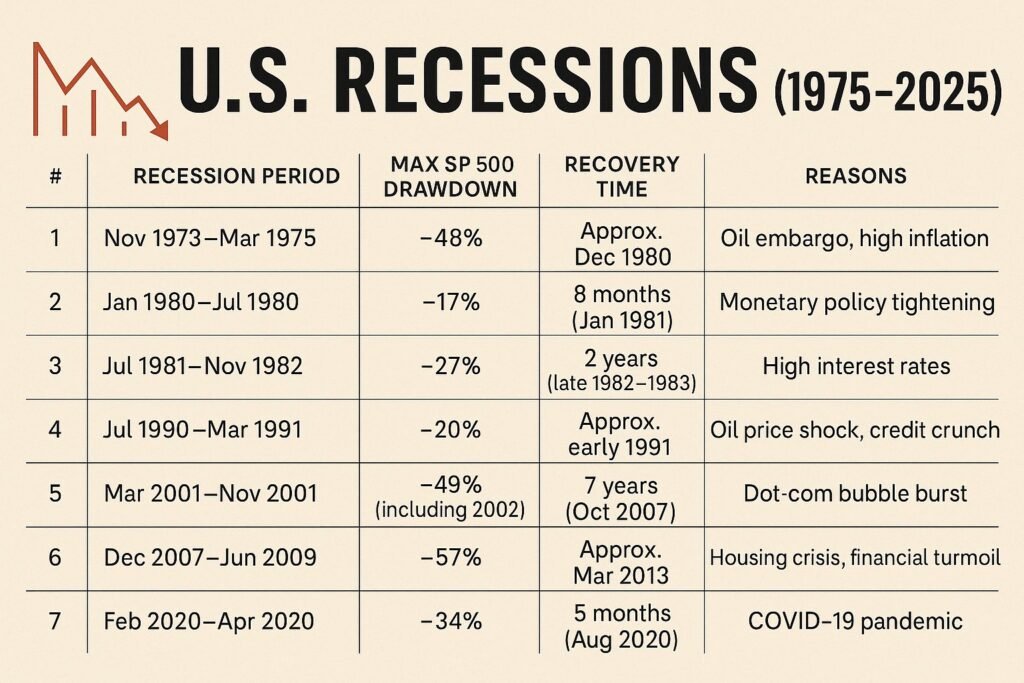

- S&P 500 Drawdown: Nearly –48%

- Recovery Time: Took about 7 years to reclaim pre-recession highs.

- Notable Quote: “WIN buttons” (Whip Inflation Now) were passed out like candy. The idea came from President Gerald Ford, who hoped citizens would voluntarily fight inflation by saving money, avoiding unnecessary spending, and generally being model economic participants. Spoiler: They didn’t work—and became a punchline almost immediately.

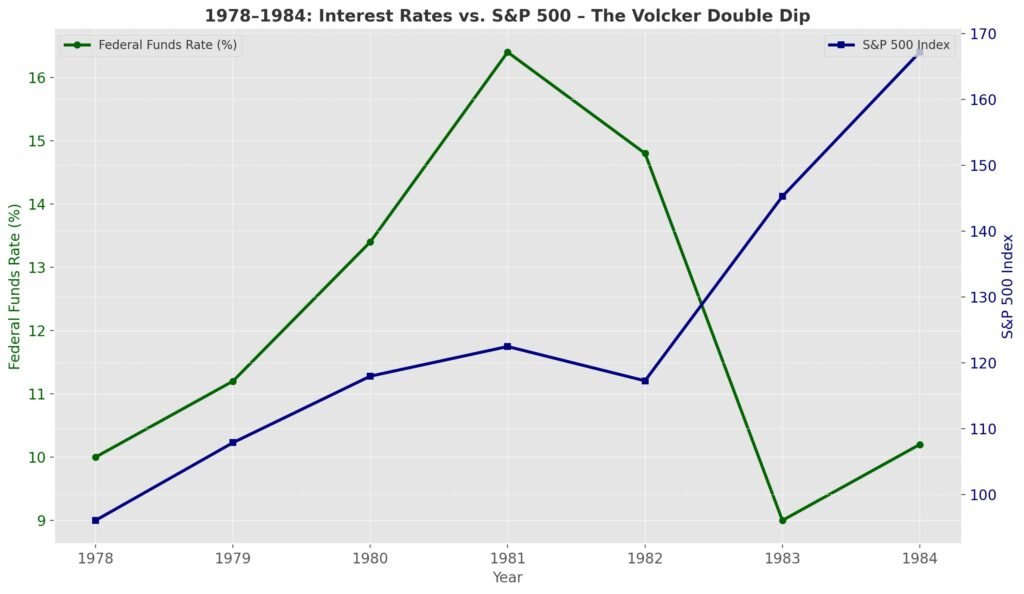

1980 and 1981–82: The Volcker Double Dip

The 1980s started with a Fed-induced recession so nice, we did it twice.

- Causes: Paul Volcker’s war on inflation. Inflation had soared into double digits in the late 1970s, eroding purchasing power and shaking confidence in the dollar. To crush it, Volcker—then Chairman of the Federal Reserve—implemented aggressive interest rate hikes. The federal funds rate spiked to nearly 20%, leading to a sharp contraction in borrowing and investment. Unsurprisingly, this triggered not one, but two back-to-back recessions

- S&P 500 Drawdown: Roughly –27%

- Recovery Time: About 2 years, with a powerful bull market on the other side. After inflation was tamed and rates were gradually lowered, the economy rebounded sharply. Businesses resumed investment, consumer confidence returned, and a long expansion period began in the mid-1980s.

Fun fact: Mortgage rates hit 18% in 1981. That’s not a typo. People still bought houses—because, apparently, fear wasn’t invented yet.

1990–91: The Forgotten Recession

A mild recession with a short memory—except if you worked in real estate or banking.

- Causes: Gulf War oil shock, S&L crisis aftermath, and tight credit conditions. The invasion of Kuwait by Iraq in 1990 caused a sharp spike in oil prices, reigniting inflation fears. Meanwhile, the Savings and Loan (S&L) crisis left many banks weakened and risk-averse, choking off credit to consumers and businesses. Add in a post-boom hangover from the 1980s debt-fueled growth, and the economy took a cautious pause.

- S&P 500 Drawdown: Around –20%

- Recovery Time: Less than a year. Once oil prices stabilized and the Fed eased monetary policy, the recovery began to take hold, helped along by a tech-fueled productivity surge that would soon define the 1990s expansion.

This was the “soft landing” recession before soft landings were cool.

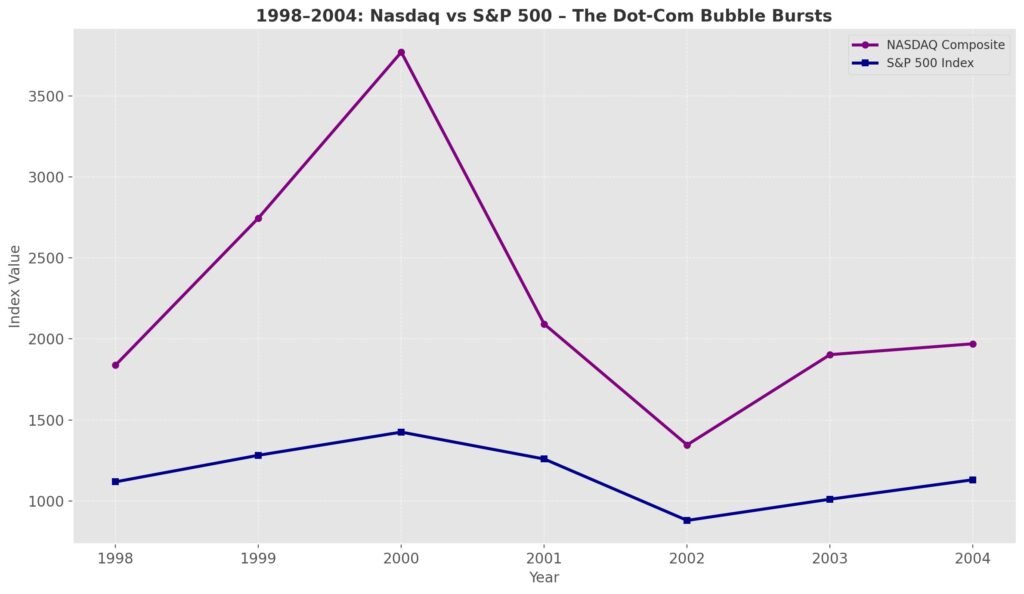

2001: The Dot-Com Bubble That Went Pop

Tech investors in the late ’90s thought profits were optional. Turns out, they’re not.

- Causes: Dot-com crash, 9/11 attacks, and corporate accounting scandals (Enron, anyone?). In the late 1990s, a speculative mania over internet stocks pushed valuations to absurd levels—companies with no revenue or viable business models were suddenly worth billions. When reality set in, the bubble burst spectacularly in 2000, dragging down the Nasdaq by nearly 80%. The final blow came with the terrorist attacks of September 11, 2001, which froze consumer spending and corporate activity, leading to a sharp but relatively short-lived recession.

- S&P 500 Drawdown: Roughly –49%

- Recovery Time: Nearly 7 years to bounce back. The S&P 500 didn’t return to its previous peak until 2007, as tech stocks took years to recover. Meanwhile, the Federal Reserve slashed interest rates, and the Bush administration passed significant tax cuts to help stimulate demand and restore confidence.

2007–2009: The Great Recession (a.k.a. Wall Street’s Midlife Crisis)

If this one had a movie title, it’d be Too Big to Fail: The Sequel You Didn’t Ask For.

- Causes: Subprime mortgage collapse, Lehman Brothers bankruptcy, and a broken financial system. In the early 2000s, low interest rates and lax lending standards fueled a housing bubble of epic proportions. Banks issued risky subprime mortgages and repackaged them into opaque financial products sold around the world. When home prices fell and borrowers began defaulting, the entire financial system was caught off guard. Lehman Brothers collapsed, triggering a full-blown global financial crisis that froze credit markets and sent consumer confidence into a nosedive.

- S&P 500 Drawdown: A stomach-churning –57%

- Recovery Time: 4.5 years, with help from massive bailouts and stimulus packages. The U.S. government responded with the $700 billion TARP bailout to stabilize banks, and the Federal Reserve slashed interest rates to zero and launched multiple rounds of Quantitative Easing (QE). Fiscal stimulus came in the form of the American Recovery and Reinvestment Act of 2009, aimed at infrastructure, tax relief, and direct payments. While the recovery was slow and uneven, the S&P 500 eventually rebounded and began a decade-long bull run.

The Fed cut rates to zero, launched QE, and even saved GM. It was like Oprah: “You get a bailout! And you get a bailout!”

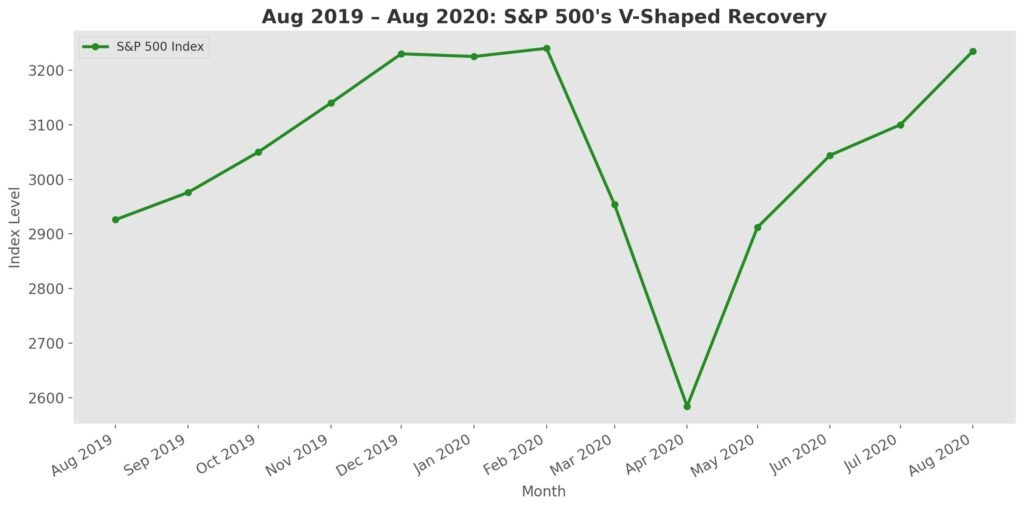

2020: The COVID-19 Crash (Shortest. Recession. Ever.)

Blink and you missed it. But your portfolio probably didn’t.

- Causes: Global pandemic, lockdowns, and an economic shutdown that halted entire industries overnight. In early 2020, COVID-19 swept across the globe, prompting governments to impose strict lockdowns to contain the virus. Travel, dining, entertainment, and retail sectors came to a sudden halt. Unemployment soared as businesses shuttered temporarily or permanently. Although the underlying financial system remained intact, the abrupt stop in consumer and business activity caused the sharpest GDP decline in U.S. history.

- S&P 500 Drawdown: –34% in just a few weeks

- Recovery Time: 5 months — the fastest on record. The rapid rebound was powered by massive fiscal stimulus, including direct checks to households, expanded unemployment benefits, and forgivable loans to businesses. The Federal Reserve slashed interest rates to zero and pumped trillions into the financial system, calming markets and boosting liquidity almost overnight.

With trillions in stimulus and rates near zero, the market acted like nothing happened—because in a way, everything happened too fast to process.

Wait, What About 2023–2025?

As of this writing, the U.S. hasn’t had an official NBER-declared recession since 2020—but it’s complicated.

Rising interest rates, inflation spikes, and volatile markets have created recession vibes. Adding fuel to the fire, investors are now bracing for potential fallout from proposed reciprocal tariffs floated by President Trump—targeting countries like China, Vietnam, and Germany. Critics warn these tariffs could disrupt global supply chains, raise consumer prices, and potentially act as a self-inflicted economic headwind just when stability seems within reach. So far, no official declaration—but investors remain on edge.

Stay tuned. Economies never stay calm for long.

What Causes US Recessions?

Recessions can be triggered by a variety of culprits—some classic, others more creative.

- Monetary policy is a frequent suspect: aggressive interest rate hikes by central banks (think Volcker in the 1980s or Powell more recently) often cool inflation, but sometimes also smother growth.

- Oil shocks are another repeat offender, typically sparked by geopolitical tensions or supply disruptions that send energy prices skyrocketing—like in 1973 and 1990.

- Asset bubbles deserve honorable mention. When speculation runs wild—whether in dot-com stocks, housing markets, or crypto meme coins—it usually ends with a sharp correction and some humbled investors.

- Then there are global events: wars, pandemics, and financial panics that seem to spread faster than bad TikTok trends.

- And now, we can add trade disruptions to the list in more recent times. With new rounds of proposed tariffs on global trading partners, concerns are rising that economic nationalism could tip fragile economies into recession, especially if retaliation follows.

In short: if it’s big, unpredictable, and expensive, there’s a good chance it can trigger a downturn.

What Can Investors Do?

Investing during a recession feels a bit like grocery shopping when you’re hungry—risky, irrational decisions are likely. But with the right plan, downturns can become opportunities rather than disasters.

- Stick to the plan: If you’re investing for long-term goals, don’t let short-term panic dictate your next move. History has shown time and again that markets recover.

- Diversify smartly: Defensive sectors like Consumer Staples, Health Care, and Utilities tend to hold up better when the economy slumps. They’re boring, yes—but boring is beautiful when everything else is falling apart.

- Dollar-cost average: Keep investing steadily over time. It’s less stressful than trying to time the bottom and more effective than staring at red charts while doomscrolling.

- Keep some dry powder: Holding a bit of cash gives you the flexibility to take advantage of market discounts—or just sleep better at night.

- Rebalance thoughtfully: Always check if your risk tolerance and portfolio are still in sync. Remember to balance before the worst happens.

- Ignore the noise: Headlines will scream. Twitter will panic. Your group chats will turn into CNBC. Stay calm.

Final Thoughts: Recessions Are Inevitable—Panic Isn’t

The history of US recessions shows one undeniable truth: the economy stumbles, but it always gets back up.

You don’t need to predict the next downturn. You just need to prepare for it. Diversify, stay calm, and don’t let major news headlines derail your long-term plan.

Because if there’s one thing scarier than a recession, it’s panic-selling at the bottom… and then buying back in at the top.