A few weeks ago we covered the announcement of Trump’s 25% tariffs on imports from Canada and Mexico, alongside a 10% tariff on Chinese goods. Now, a few days later on February 10, 2025, President Donald Trump announced a 25% tariff on all imported steel and aluminum, reinstating and expanding the previous tariffs implemented during his first term. The move is aimed at protecting American industries, ensuring national security, and addressing trade imbalances caused by what Trump calls “unfair trade practices.”

With these new tariffs, importers will face higher costs, forcing manufacturers and industries reliant on these metals to reassess their supply chains. The administration argues that these tariffs will encourage domestic production, preserving American jobs and reducing reliance on foreign metals, particularly from China, Canada, and Mexico. However, critics warn that these tariffs could lead to higher prices for consumers and potential retaliatory trade actions.

Domestic Steel and Aluminum Consumption: How Much Do We Produce and Import?

Understanding the U.S. steel and aluminum supply chain is key to evaluating the impact of the new tariffs. While the U.S. has strong domestic steel production, it remains heavily dependent on aluminum imports.

Steel Production and Imports

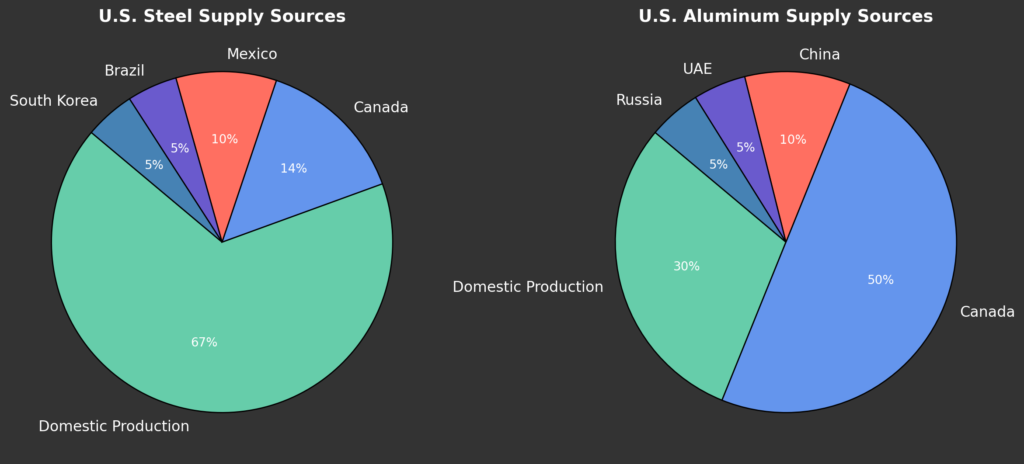

- The U.S. produces about 70-75% of its steel needs domestically.

- The remaining 25-30% is imported, primarily from Canada (14%), Mexico (9%), Brazil (5%), and South Korea (5%).

- The U.S. has sufficient iron ore reserves and steelmaking capacity to become self-sufficient if domestic production is increased.

Aluminum Production and Imports

- The U.S. only produces 30-35% of the aluminum it consumes.

- The majority—65-70%—is imported, primarily from Canada (50%), China (10%), the UAE (5%), and Russia (5%).

- Unlike steel, aluminum production is highly energy-intensive and relies on imported bauxite ore, which is not abundant in the U.S.

While the U.S. steel industry is well-equipped to scale up production, aluminum presents a greater challenge due to its reliance on foreign raw materials and smelting operations.

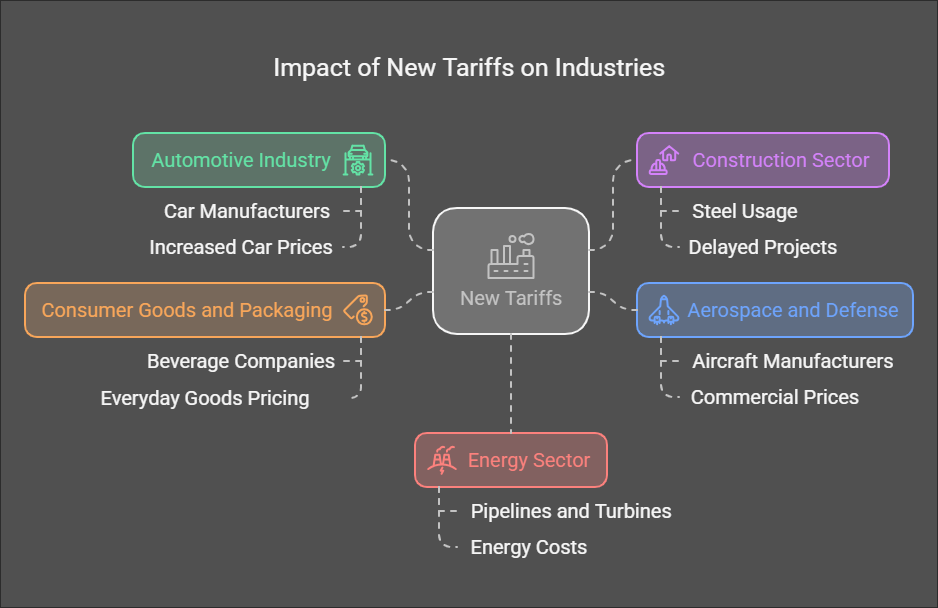

Industries Most Affected by the New Steel and Aluminum Tariffs

The 25% tariff will have effects across multiple industries that heavily rely on imported steel and aluminum. Sectors most impacted include:

1. Automotive Industry

- Car manufacturers like Ford, General Motors, Toyota, and Tesla rely on aluminum and steel for vehicle production.

- Higher material costs may result in increased car prices for consumers.

2. Construction Sector

- Steel is widely used in commercial and residential buildings, bridges, and infrastructure, impacting major companies such as Caterpillar, Nucor, and Turner Construction in the construction and materials sectors.

- Increased costs may slow down construction projects or lead to higher housing prices.

3. Aerospace and Defense

- Aircraft manufacturers like Boeing and Lockheed Martin depend on high-purity aluminum.

- Increased costs could impact defense contracts and commercial aircraft pricing.

4. Consumer Goods and Packaging

- Beverage companies like Coca-Cola, Anheuser-Busch, PepsiCo, and Ball Corporation rely on aluminum for cans and packaging.

- A rise in aluminum costs could increase the prices of everyday goods.

5. Energy Sector

- Steel is essential for pipelines, wind turbines, and drilling rigs, impacting companies such as ExxonMobil, Chevron, NextEra Energy, and General Electric.

- The tariffs could increase costs in oil, gas, and renewable energy infrastructure.

Consumers can expect price hikes in products ranging from vehicles and homes to beer cans and appliances.

Lessons from 2018: Steel and Aluminum Tariff Impacts on Inflation

A Federal Reserve study (2019) found that the 2018 steel and aluminum tariffs had minimal impact on overall inflation. Industries mostly absorbed higher costs, reducing direct consumer price hikes. However, specific sectors, such as automobiles, construction materials, and appliances, experienced localized price increases. Additionally, job gains in steel production were offset by job losses in industries that rely on steel and aluminum. While history suggests broad inflationary effects may be limited, the higher 2025 tariffs, especially on aluminum, could have a more significant impact.

Can the U.S. Meet Its Own Steel and Aluminum Needs?

While the U.S. can technically meet its steel demand, aluminum is a different story.

Steel: Self-Sufficiency is Possible

The U.S. has the iron ore reserves, facilities, and workforce to ramp up steel production, with domestic mines producing approximately 48 million metric tons of iron ore annually, primarily from Minnesota and Michigan. The U.S. steel industry operates at around 75-80% capacity utilization, indicating potential room for increased production if demand rises. However, increased domestic production takes time and investment, meaning short-term supply constraints may arise, making it challenging to quickly replace imported steel in response to sudden demand surges.

Aluminum: A Different Challenge

The U.S. lacks enough bauxite reserves and relies on imports for primary aluminum production. High energy costs make domestic aluminum smelting less competitive, as the process requires up to significant amounts of energy. Even with increased recycling efforts, which currently provide 70-80% of the U.S. aluminum supply, the U.S. cannot fully replace imported aluminum, as high-purity aluminum for aerospace and defense applications still depends on primary aluminum imports.

Results of Trumps first Steel and Aluminum Tariffs Domestic Production

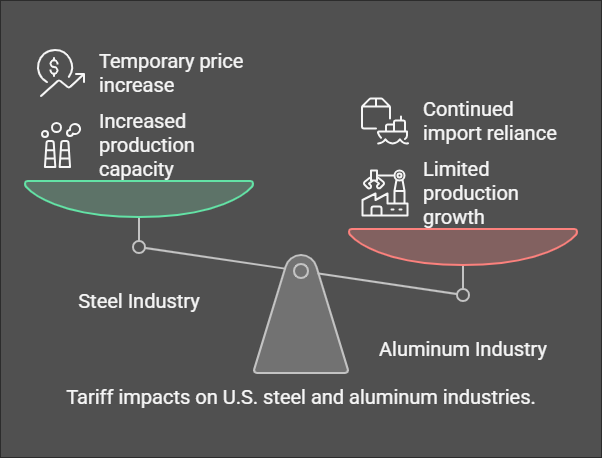

Steel Industry (2018 Tariffs)

- Capacity utilization rose to over 80%, boosting domestic steel production.

- New steel plants opened, and companies like Nucor and U.S. Steel expanded operations.

- Prices temporarily increased, benefiting steelmakers but straining industries that rely on steel.

Aluminum Industry (2018 Tariffs)

- Despite tariffs, U.S. aluminum production did not significantly increase.

- Energy costs and lack of raw materials made domestic aluminum less competitive.

- The aluminum sector remained reliant on imports, primarily from Canada.

Comparing the 2025 Tariffs vs. the 2018 Tariffs

The 2025 tariffs differ from the 2018 tariffs in key ways:

| Factor | 2018 Tariffs | 2025 Tariffs |

|---|---|---|

| Rate | 25% steel, 10% aluminum | 25% steel, 25% aluminum |

| Countries Targeted | Exemptions for Canada, Mexico, EU | No exemptions—applies to all imports |

| Goal | Increase U.S. production | Strengthen domestic supply chains & reduce foreign dependence |

| Effect on Industry | Benefited steelmakers, minimal aluminum impact | May have stronger aluminum effects but risks higher consumer prices |

The 2025 tariffs are harsher on aluminum imports, which could incentivize recycling and production investments. However, they may increase consumer prices and provoke trade retaliation.

How Can U.S. Companies Source More Domestic Aluminum?

Given that the U.S. lacks significant bauxite reserves and primary aluminum production is costly and energy-intensive, companies must explore alternative strategies to secure more domestically sourced aluminum. Here are key solutions:

1. Expand Domestic Aluminum Recycling (Secondary Aluminum)

One key approach is expanding domestic aluminum recycling, as the U.S. already meets 70-80% of its aluminum demand through recycling. Increasing collection and processing facilities could further reduce reliance on imported primary aluminum, though it requires investment in sorting technology and consumer participation in recycling programs. Expanding these efforts could significantly reduce the need for high-carbon primary aluminum production.

2. Reopen and Upgrade Domestic Smelters

Reopening and upgrading domestic smelters is another viable solution. The U.S. currently has only five operational aluminum smelters, down from 23 in 2000. Restarting idled smelters, such as those operated by Alcoa and Century Aluminum, could boost supply. However, high electricity costs pose a significant challenge, as aluminum smelting is energy-intensive. Incentives for renewable-powered smelters, including those using hydropower, nuclear, or solar energy, could help lower costs and make domestic production more competitive.

3. Develop Alternative Aluminum Sources

Developing alternative aluminum sources could also help reduce dependency on imports. Research into processing aluminum from clay deposits in states like Arkansas and Georgia could provide a domestic alternative to bauxite-based aluminum production. However, this technology is still in early-stage development and is not yet commercially viable.

4. Encourage U.S.-Based Manufacturing Partnerships

Encouraging U.S.-based manufacturing partnerships can also help strengthen domestic aluminum supply chains. Automakers and aerospace firms such as Ford, GM, and Boeing can invest in domestic recycling programs and sustainable aluminum sourcing. Additionally, government incentives such as tax breaks or subsidies for companies prioritizing U.S.-produced aluminum over imports can further drive local production. Forming partnerships with domestic suppliers like Alcoa and Century Aluminum could also help increase local processing capacity

5. Invest in Energy Efficiency and Smelting Technology

Lastly, investing in energy efficiency and smelting technology will be crucial for long-term sustainability. New smelting techniques, such as inert anode technology being developed by Alcoa and Rio Tinto, can reduce energy use and emissions. Additionally, transitioning existing plants to hydropower-driven production could make U.S. aluminum more cost-competitive. Lowering production costs through innovation could help reduce dependence on foreign imports over time.

Conclusion

Trump’s new 25% tariffs on steel and aluminum are intended to boost domestic production and reduce foreign dependence. While the U.S. can meet its steel demand, aluminum remains heavily import-dependent, making the effects of the tariffs more uncertain.

The 2018 tariffs boosted steel production, but aluminum production barely increased due to high energy costs and limited bauxite reserves. The 2025 tariffs are broader and more aggressive, impacting industries from automotive to packaging and potentially raising consumer prices.

Ultimately, the success of these tariffs depends on whether domestic steel and aluminum production can scale fast enough to replace imports. If not, the U.S. may see higher prices, retaliatory tariffs, and continued reliance on foreign metals.

[…] imports 60% of its aluminum and about 15% of its auto-grade steel, both now subject to revived Trump-era tariffs (25% on steel, 10% on aluminum). This raises costs for automakers regardless of where they build vehicles, since U.S.-based plants […]

[…] Trump’s first tariff offensive. During his first term, he imposed major tariffs on steel and aluminum, as well as $250 billion worth of Chinese goods under Section […]